Active Managers – Do They Pass or Fail in Equities?

“Yes, the world is out to get active managers” − Bloomberg

“But a challenging year for active managers” − Bank of America Merrill Lynch

“An active headache for fund managers” − Financial Times

“Investors losing faith in active managers” − The Irish Times

“Active management stunk in 2014!”

Last year marked the worst year (since 2003) for active large-cap managers beating the Russell 1000. In 2014, 80-90% of active U.S. equity managers under-performed their respective benchmarks in 2014. The headlines listed above point towards a possible exit for active management.

The herd migrates.

Such data could make investors jump to conclusions, fully embrace passive management, and buy nothing but index funds; after all, why would any investor bother with the time, headache and cost of under performing active managers? That is exactly what happened. Morningstar data shows that $166.6 billion flowed into passive (index) U.S. equity funds in 2014 and $98.4 billion flowed out of actively managed equity funds. Including international equity funds, a net $420 billion flowed into passive equity funds, while just $44 billion flowed into actively managed funds,

about a 10-to-1 funding ratio, making indexing one of the biggest stories in recent times!

The Human Factor:

Some investors have gone passive chasing performance, which begs the question, are they looking for instant gratification or are they really committed to low-cost passive indexing? James Grant, editor of Grant’s Interest Rate Observer, argues that passive investing has become a risky fad. While investors flow out of active U.S. equity managers, other investors continue to pump money into pricier active alternative asset class managers. We understand that it can be difficult for investors to stick to active management when large cap U.S. equity active managers have underperformed for extended periods. Our human brains are hardwired to seek near-term happiness and use the experience of recent failures to make decisions. Despite the lopsided results and flight to passive, there is plenty of work to be done before concluding that active managers offer no value in any asset class or any market environment.

So, before you extrapolate from short-term results and show active managers the door, let’s explore the active vs. passive debate more critically and research where indexing has worked and where it has not. Our analysis, outlined below, leads us to conclude that a blend of both active and passive managers works most effectively.

Where indexing works.

When the markets are rallying, indexing works because you get to participate in the up. The bull market of the last six years (2009−present) has been a perfect environment for passive indexing in large-cap U.S. equities – especially if you owned the S&P 500! Indexing also seems to work in those asset classes where information flows freely and the markets are more efficient, both of which accurately describe the large-cap U.S. equities market. Indexing’s other value propositions include: broad diversification; low-cost exposure to the market; market-like returns; and in many cases, greater tax-efficiency. Indexing also offers investors easy access to the market as conducting intensive due diligence to find good active managers can be expensive and time-consuming.

Where indexing does not work.

What indexing does in an up market, it also does on the way down. If the markets are dropping, index investors can expect to receive the full brunt of the market downturn. Generally, if the possibility of downturn seems strong, it may be wise to accept the active managers’ promise of a better risk-adjusted performance than index funds typically deliver. We enter 2015 during the third longest uptrend in market history. (The longest ended in 1929 and the second longest ended in 2000.)

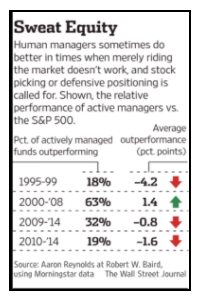

Source: Morningstar.

Active managers tend to make up lost ground when markets level off or suffer corrections. The chart shows that when the market was trading sideways (as it was in 1995-1999), or straight up (like 2009/2010-2014), active managers lagged. However, from 2000-2008, nearly two thirds of active large-cap fund managers beat the S&P 500 by an average of 1.4 points annually.

Source:Wall Street Journal

The lesson here? Historically, active managers have lagged behind benchmarks during long, strong bull markets, when securities selection makes less of a difference. The human factor strikes here again as investors often find it difficult to suffer underperformance during up markets; investors must be patient and wait for periods when active managers may excel.

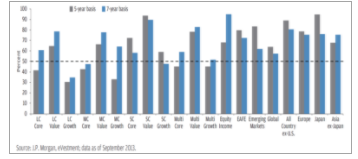

>While the challenges over the last few years have been greatest for U.S. large-cap growth managers, active managers have had greater success in other asset classes. The chart illustrates historical 5 and 7 year active manager outperformance trends over their respective ETFs. They have shown better long-term performance in less efficient marketplaces like International, Emerging, and Small-Cap markets, where they may have an information advantage and thus more opportunities to benefit from market mispricing. Less efficiency also implies that skill can play a relatively larger role than luck. While short-term performance might be attributable to luck, the long-term performance of an active manager is often more about skill. The process of finding skilled active managers is critical to the success of active management.

Indexing also has its flaws inherent to the market indexes being replicated. Market-cap weighted indexes such as the S&P 500 and the Dow Jones Industrial Average buy more of the bigger company stocks and fewer shares of smaller ones, which can distort the diversified indexes, especially during market peaks. The cap weighting links the weight of a holding in the index to its price, so the more expensive a stock gets, the bigger its weight in the index. For example, in early 2000, about 50% of the S&P 500 was in soaring tech stocks (right before the tech bubble burst), and in early 2008, about 40% was in high-flying financial stocks (right before the mortgage crisis hit). When the market corrected, this weighted index was hit hard.

Source:Navellier.

Our View:

There are merits to passive investing. And there are merits to active investing. We are proponents of blending the two; we firmly believe that combining active and passive strategies provides a superior risk-return profile than exclusively using active or passive strategies alone.

In our opinion, both ‘all-active’ and ‘all-passive’ approaches have serious potential flaws. Active management allows for the continuous assessment of the market and intentional choices about how best to take advantage of opportunities and mitigate risk. Passive management precludes the ability to add value in this way. Passive management offers greater tax efficiency and lower costs while giving broad market exposure. Thus, we believe a blend of both gives investors the best of both.

We think it worthwhile to share the framework and thought process we use to help remove behavioral biases while allocating to active and passive in asset classes. Our decision to invest in a blend of active and passive strategies is based largely upon the following factors: the degree of market inefficiency in an asset class, which gives active managers a potential informational advantage; the spread between index and active managers long-term historical returns; the degree of risk-enhanced returns in different market environments; and the investment process (disciplined, defined and repeatable) of active and passive managers. We also pay careful attention to the role that the investment is designed to play in the broader portfolio and how well the index is aligned with the desired capitalization profile, style profile, country exposure or credit exposure, the kind of index benchmark to use, the index products available, the spread between the returns of the indexed product and its benchmark. These criteria help us determine whether the cost and risk of active management is worth it.

Pass or Fail?

You may be disappointed by the recent performance of active managers and give them a failing grade. Regardless of the grade, we recommend reviewing this objectively, while setting aside your emotions and responses to short-term performance and headlines. While the media and experts continue their debate on whether active management is still viable, you can use an objective process to determine what works best in your portfolio. We think the above framework provides justification for using a blended approach while providing a roadmap for taking subjectivity out of the decision-making process. In our opinion, a blend of both wins.

THANK you JOYN. Article previously posted here:

Disclosures and Disclaimers:

The information provided herein is for general educational and entertainment purposes only, and should not be considered an individualized recommendation or personalized investment or financial advice; nor should the information provided herein be considered legal, tax, accounting, counseling or therapeutic advice of any kind. Any examples or characters mentioned herein are hypothetical in nature, purely fictitious, and do not reflect any actual persons living or dead. Practical Investment Consulting makes no representations, whether express or implied, as to any expected outcome based on any of the information presented herein. Users assume all responsibilities or the use of these materials, including the responsibility of protecting the privacy of their responses. Practical Investment Consulting does not accept any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this document or its contents.

This material is intended for the personal use of the intended recipient(s) only and may not be disseminated or reproduced without the express written permission of Practical Investment Consulting.